By Tanjilut Tasnuba

‘There are more mobile money accounts than adults in Kenya.’-Bill Gates

Above quote resonate with the mobile money revolution that is happening in Kenya, a fore frontier nation in digitalizing financial inclusion. Electronic money transfer through mobile money platform shows a rapid growth in the emerging markets in recent years. And for Kenya, the impact of using mobile money platform to provide financial services to all citizens across the nation has shown more than double increment in the numbers of users of formal financial services, from 26.4% of adults in 2007 to 66.7% of adults in 2013, in a span of seven years.

Case-in-point could be M-PESA, an m-payment service launched by Vodafone and Safaricom in 2007, which gained more than 2.37 million users in little over one year. Per their 2014 annual report, M-PESA have around 19 million subscribers. The success of this scale-up process and the best practices of the design of this system can be replicated in other countries who are trying to capitalize on the mobile money platform to foster the financial inclusion process.

As for Bangladesh, it has already started to capitalize on the mobile money technology to move towards a cashless future. bKash, the second largest mobile money service provider, sets out a comprehensive mobile money network with widespread active agents and shows 16.5 million active subscriber with an average of $47.44 million daily transaction (May, 2015). However, it is eminent for bKash and likewise organization to know the standard operational procedure of this industry to actually move towards cashless future and materializing the vision of financial inclusion. On that front, the following three key takeaways from my visit to Nairobi, Kenya would be influential for us as we are as a nation, stepping towards creating an enabling mobile money platform:

Takeaway one: Regulatory transparency

The Central Bank of Kenya (CBK) plays a catalytic role in developing an ecosystem for Kenya to leapfrog access to financial services. The core focus of the Bank has been to create an enabling legal and regulatory environment with a factual knowledge of the business models along with the nature of the risk, and appropriate risk measurements. Capitalizing on this comprehensive friendly ecosystem M-PESA has been integrated to different service providers to ensure efficient financial transactions. Few examples include: government payments, ticket purchase, savings, buying airtime, buying goods and of course sending money.

Case-in-point could be Musoni and Bridge International Academies who are using M-PESA platform to achieve operational excellence.

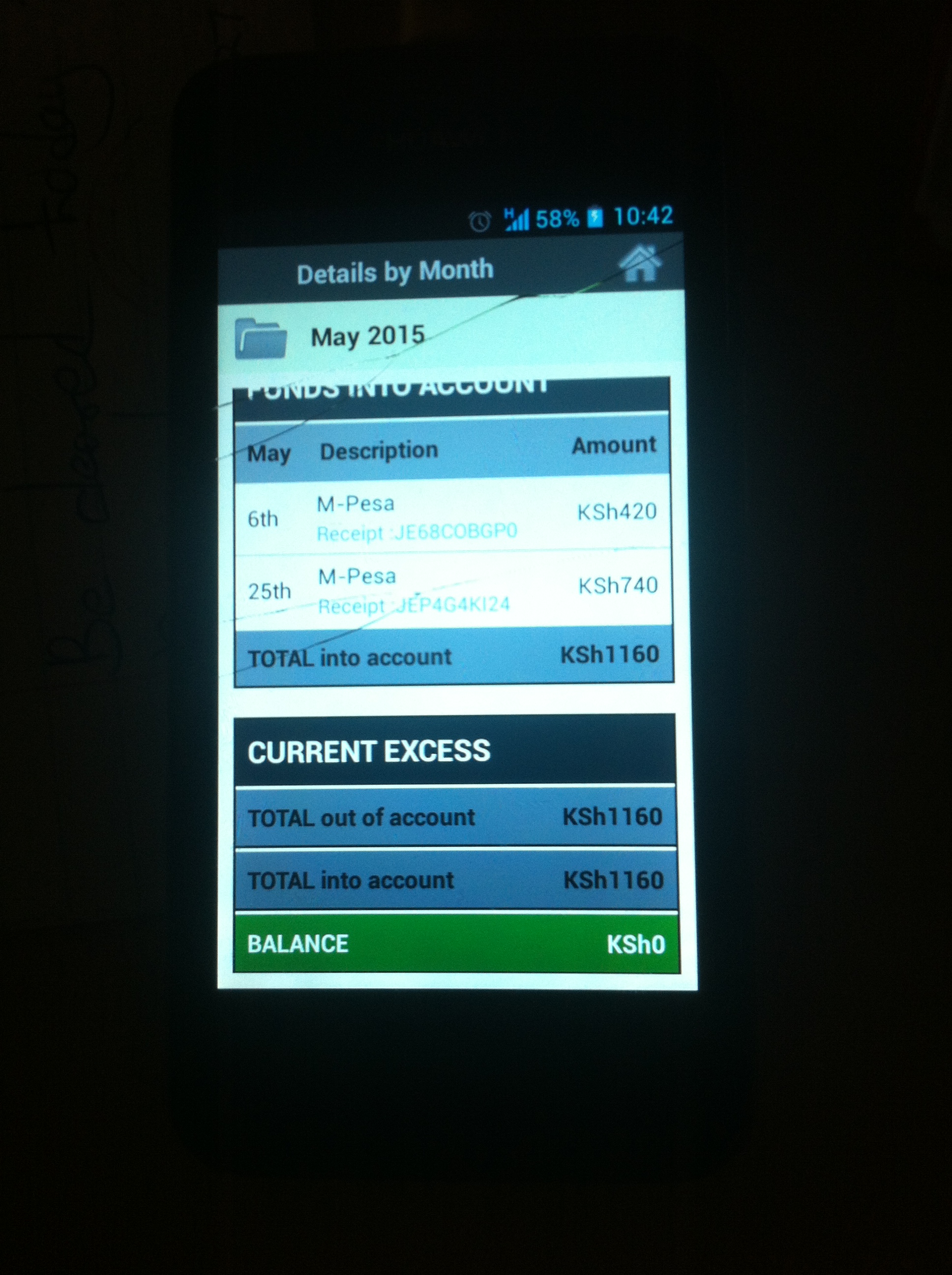

Musoni, a microfinance service provider, which places mobile money platform at the core of its business model. All transaction of Musoni takes place through M-PESA platform. Using the services of M-PESA, Musoni ensures credit disbursement within 24 hours of getting the demand and collect the installments as well. Moreover, it also integrates other sensitive factors related to ensuring transparency of the system such as client information collection, monitoring and evaluation through using the platform of M-PESA.

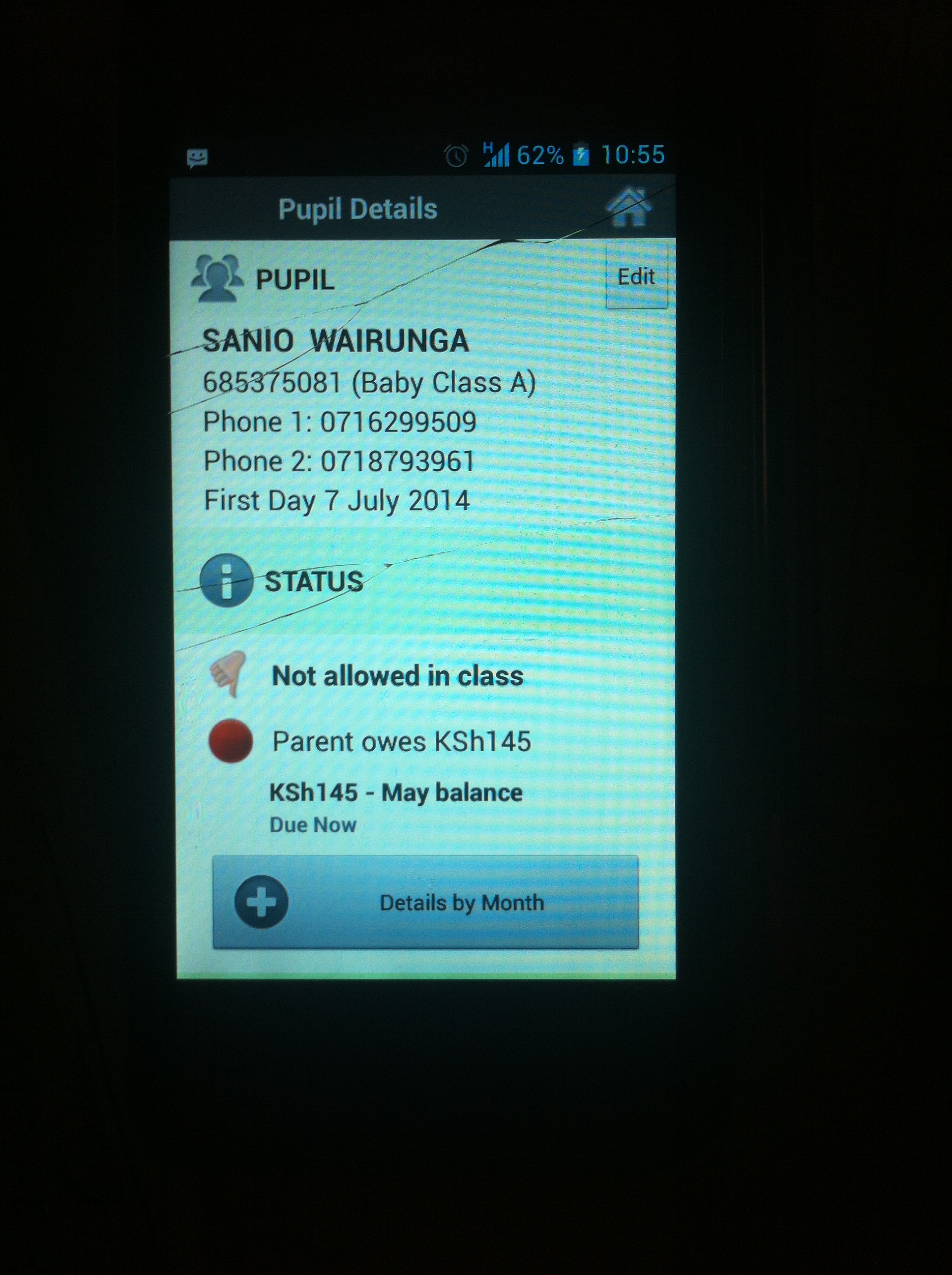

Bridge International Academies, the world’s largest chain of primary and pre-primary schools, have a cashless operation system using M-PESA platform to manage all kinds of financial transaction ranging from salary and tuition fee disbursement to product purchase by students.

Takeaway two: Empowering other stakeholders

To get the best out of the mobile money platform, it is paramount to have a sound know-how on the technical aspects of the entire value chain of the process . All stakeholders of this ecosystem ranging from central bank to network operators need to well acquaint with the system. Safaricom provides these training its entire stakeholder in an effect of relentless pursuit for excellence. Helix Institute of Digital Finance is such another training institute that provides customized trainings to mobile network operators, banks, financial institutions, and third party providers.

. All stakeholders of this ecosystem ranging from central bank to network operators need to well acquaint with the system. Safaricom provides these training its entire stakeholder in an effect of relentless pursuit for excellence. Helix Institute of Digital Finance is such another training institute that provides customized trainings to mobile network operators, banks, financial institutions, and third party providers.

Takeaway three: Intervention through Innovation

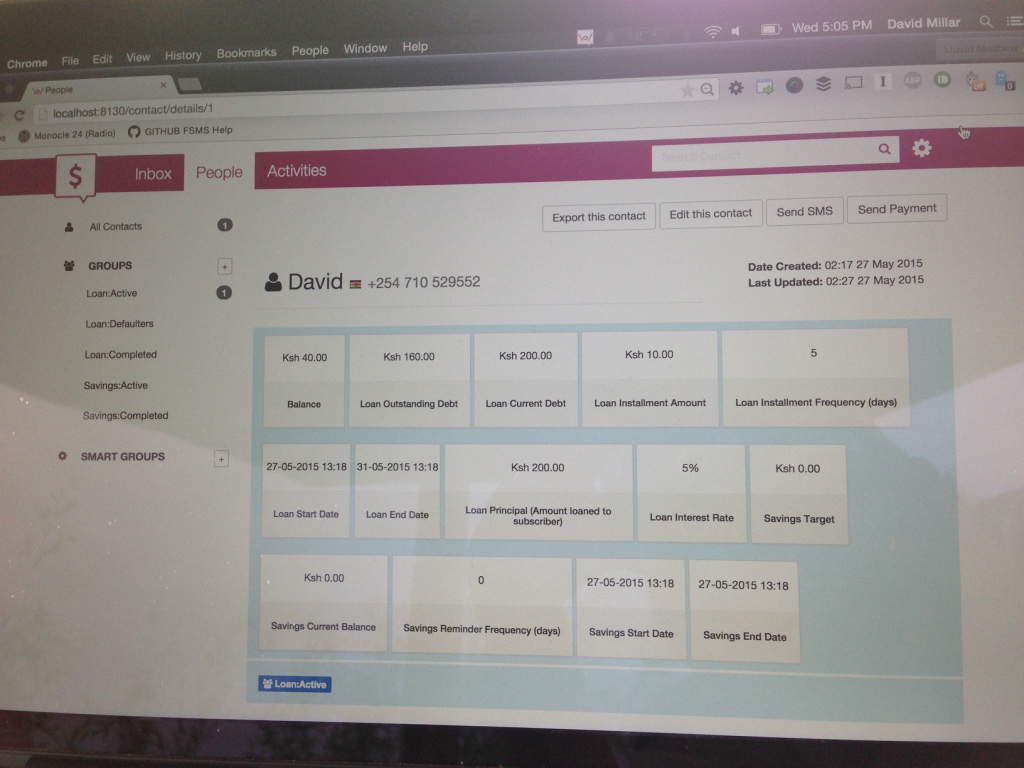

The tech innovation that is needed to support the high-tech model of mobile money intervention is already there in Kenya. Mobile money as a tool alone could not make such triumph in Kenya if it did not have the back end support made by organizations like Frontline SMS. These tech organizations are continuously working on making easier back-end solutions for the organizations and use cases for the easier operations with mobile money.

In bringing mobile money platform to the mainstream financial service, Kenya sets the benchmark for others. In the long run, Bangladesh can learn from the above best practices of the design of the whole ecosystem of Kenya’s mobile money revolution. Kenya’s mobile money revolution is nothing but a major milestone towards achieving its vision of 2030, where it has been clear sets out the significance of having a deeper and broader financial sector. However, a vision cannot materialize by itself. It require combine effort from public, private, and civil sector to make it real, in this case Kenya did it successfully.

This transformation in Kenya didn’t happen in a day. After visiting iHub– the innovation hub of Nairobi, I would say,

“Mobile money is not just a system of money transaction. It has a huge potential to make the whole system efficient. It is just a matter of looking at it with a vision.”

Tanjilut Tasnuba is a Deputy Manager with the BRAC Social Innovation Lab.